Introduction

In the world of finance, keeping a close eye on various indicators is crucial for investors. Recently, two significant developments have captured the attention of the financial community: the VIX futures slipping into backwardation and the gradual normalization of the US Treasury yield curve, particularly the 2-10 portion. Both of these developments have important implications for investors. In this blog post, we’ll delve into the reasons behind these occurrences and why they matter to investors.

Understanding VIX Futures Backwardation

Before we dive into VIX futures backwardation, it’s important to understand the concept of futures curves. In normal times, the shapes of the VIX futures and US Treasury yield curves tend to resemble each other, both sloping upwards from left to right. The reason behind this similarity is rooted in the nature of interest rates. Bond investors typically demand higher yields for longer-dated bonds as they are more sensitive to changes in interest rates, making them more volatile. Investors generally prefer less volatile instruments, so they are willing to pay higher prices for shorter-term bonds.

Futures curves typically have an upward slope due to advantageous margin requirements. This means that investors can control a certain amount of a commodity while using only a small percentage of the money required to buy it when the futures contract expires. The unused money can be invested in risk-free assets, such as T-bills, which creates the upward slope in the futures curve. Nearer-term futures usually have lower prices than their longer-term counterparts, a condition called contango. The opposite situation is called backwardation.

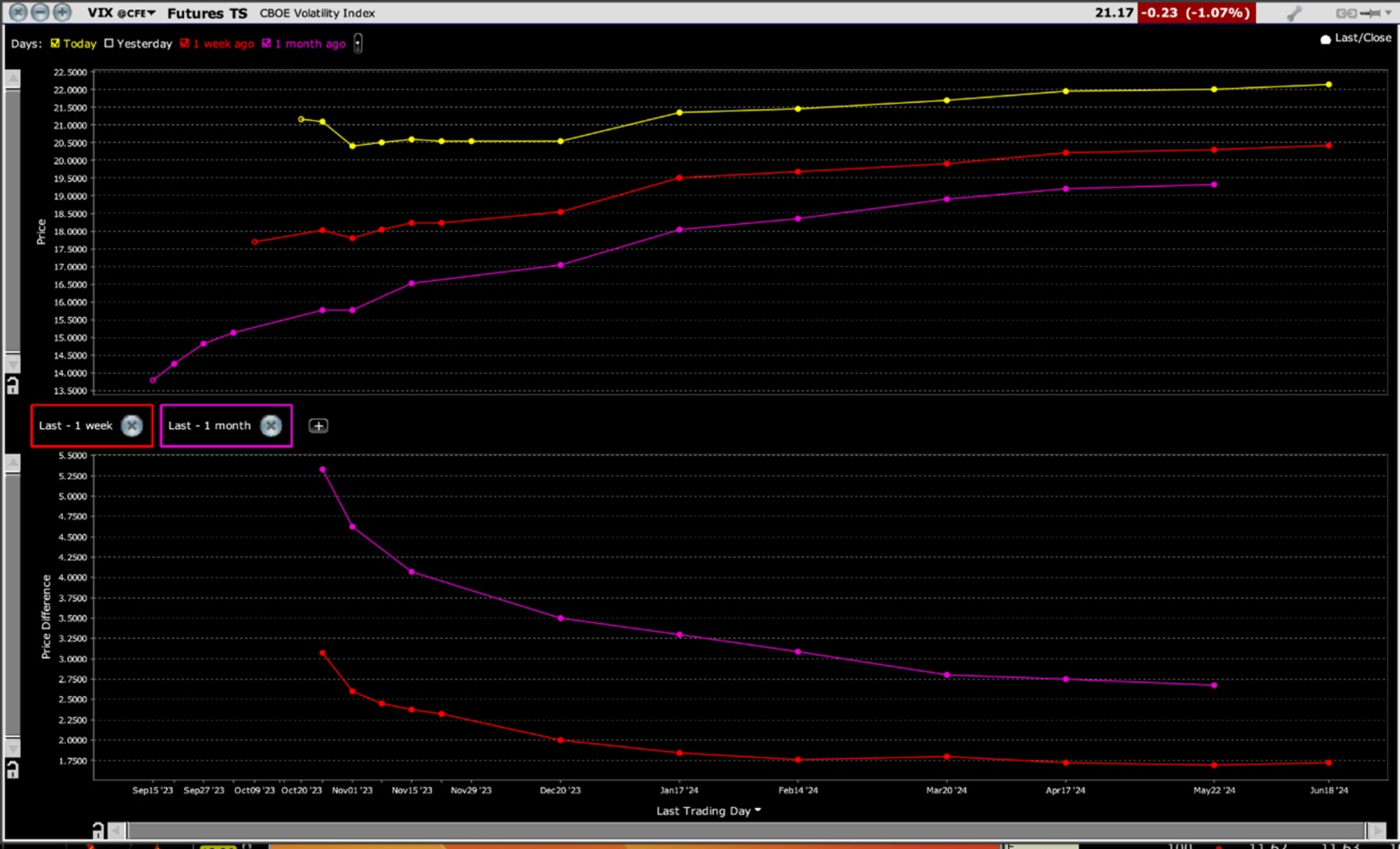

Backwardation occurs when the near-term demand for a commodity outstrips the supply. In the case of the VIX (Cboe Volatility Index), it’s a measure of volatility protection. Over the past year, despite various market uncertainties, volatility was in ample supply. However, recent demand for volatility protection has surged, and the futures curve has flipped into backwardation, indicating a change in market sentiment.

While the backwardation in the VIX futures curve is notable, it’s not at the levels that typically signal panic. Some traders view an inverted VIX curve as a contrarian indicator, but it’s not sufficient by itself to predict a market bounce. The curve can remain in backwardation for an extended period, and sell-offs usually end when demand for protection becomes extremely high, indicating an oversold condition.

VIX Futures Term Structure, Today (yellow, top), Last Week (red, top), Last Month (magenta, top), with 1-Week (red, bottom) and 1-Month Changes (magenta, bottom)

The Yield Curve Normalizing

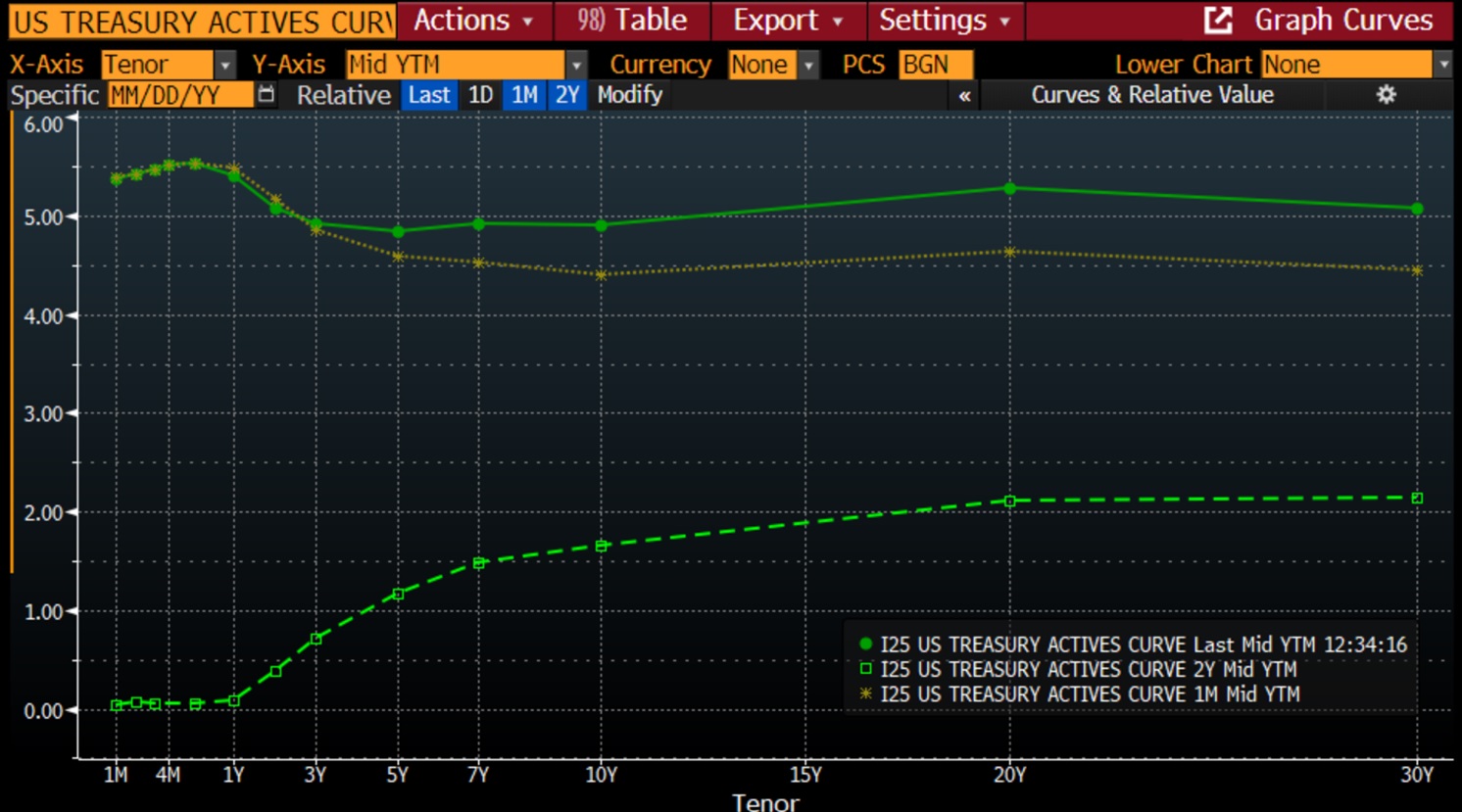

In parallel to the VIX futures curve, the US Treasury yield curve, specifically the 2-10 portion, has been inching closer to normalizing. In normal times, the yield curve slopes upwards, with long-term yields higher than short-term yields, driven by investor preference for liquidity and lower volatility. However, recent yield curve inversions have raised concerns about the possibility of an impending recession.

Historically, inverted yield curves have been strong indicators of future recessions, but it’s crucial to understand that recessions typically begin after the inversion ends. The recent yield curve data shows that while the overall level of rates was much lower two years ago, the shape of the curve is relatively normal compared to last month, suggesting an easing of the inversion.

US Treasuries Active Yield Curve, Today (green line), Last Month (yellow), 2 Years Ago (green dashes)

30 Years, 2-10 Treasury Yield Spread (blue/white bars) vs. NBER-defined Start (red) and End (green) of US Recessions

Implications for Investors

These developments may not have an immediate influence on the markets, but they can significantly affect the paths of stocks, bonds, and the economy in the coming days and weeks. Investors should remain vigilant and consider the implications of VIX futures backwardation and the yield curve normalization on their investment strategies.

In conclusion, the recent backwardation in VIX futures and the normalization of the yield curve are important indicators for investors. While they may not provide immediate signals, they serve as valuable tools to gauge market sentiment and potential shifts in the investment landscape. Staying informed and being prepared for different market scenarios is essential for making sound investment decisions in an ever-changing financial landscape.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/understanding-the-significance-of-a-vix-futures-backwardation-and-the-normalizing-yield-curve-for-investors.html