As the golden years approach, many soon-to-be retirees look forward to improved golf scores, but there’s another score that doesn’t necessarily follow the same positive trajectory: the credit score. This might seem counterintuitive; after all, shouldn’t years of diligent on-time payments, coupled with a reduction in income obligations, result in an improved credit score during retirement?

According to Ethan Dornhelm, Vice President of Scores and Analytics at FICO, it’s not quite so simple. Dornhelm explains that while the act of retirement itself does not directly impact credit scores, related lifestyle changes, such as scaling back expenses or paying off loans, can potentially affect these numbers.

The Relevance of Credit Scores in Retirement

Credit scores may seem less relevant to retirees who are not likely to apply for mortgages or other loans. However, these scores hold substantial significance in many other aspects of life, including insurance and healthcare decisions. From determining premiums to being accepted into an assisted-living facility, a good credit score can make all the difference.

As Bill Stack, a financial advisor specializing in serving seniors, notes, financial freedom in retirement ideally means not worrying about whether your score is a 790 or a 650. However, with more retired Americans still juggling mortgage debt and credit-card balances, maintaining a healthy credit score remains important.

Understanding Score Fluctuations

Credit scores are not stagnant; they can fluctuate based on several factors. Case in point, Clarence Stokes, a retired public-utility employee, saw his credit score drop from 806 to below 740 due to a single late credit card payment. Even though his overall record was impeccable, this seemingly minor incident impacted his score significantly.

As per FICO, the average score tends to rise as consumers age, peaking in the 70s at 762. After age 79, this number slightly falls to an average of 756. While retirees generally maintain healthy credit scores thanks to their long credit histories, closing old accounts, even inactive ones, can cause scores to drop. The mix of different types of loans also impacts the score, which can hurt retirees who have already paid off their mortgages and auto loans.

Surprisingly, some retirees may even find themselves without a valid credit score if their credit report hasn’t been updated in the past six months. FICO refrains from issuing scores for “stale files” due to insufficient data. However, VantageScore, a rival scoring agency, uses historical repayment data to predict future borrower behavior instead of letting credit scores go inactive.

Strategies to Maintain Healthy Credit Scores in Retirement

While the intricacies of the credit scoring system may seem daunting, there are practical ways to maintain, and even improve, your credit score in retirement. First and foremost, retirees should continue to keep credit accounts active by using them regularly, suggests Dornhelm of FICO.

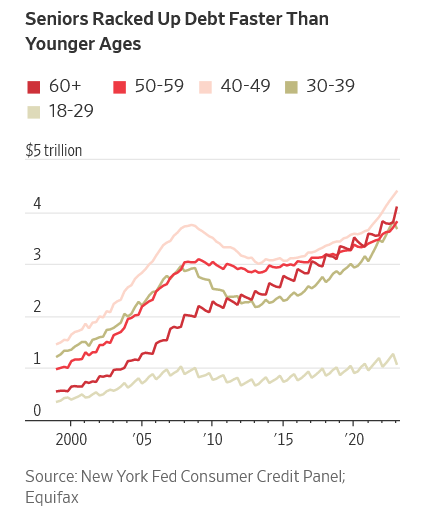

However, the reality for many retirees is that they are entering their golden years carrying more debt than ever before. Total household debt for those over age 60 quadrupled over the past two decades to $4 trillion, according to Federal Reserve data. With most senior debt tied to mortgages and credit card balances, financial advisors generally recommend that clients try to pay off as much debt as possible before retiring.

However, navigating fixed or lower income in retirement combined with higher interest rates and inflation can quickly escalate debt burdens, making them unmanageable. In these situations, understanding and working within the system is crucial. As Stokes, the retiree from Kentucky, has demonstrated, one can keep a healthy credit score and earn benefits by charging expenses onto a credit card and promptly paying them off, even when they could pay in cash.

“You can’t change the system, but if you know the system, then you can work the system,” Stokes said, reinforcing the importance of financial literacy in maintaining a healthy credit score during retirement.

In conclusion, retirement brings changes that can inadvertently impact your credit score. It is crucial to keep track of your credit score, even if you are not looking to borrow money. A solid credit score not only improves your financial standing but can also have an impact on other aspects of your retired life. By staying proactive and knowledgeable, retirees can maintain a strong credit profile, ensuring they enjoy their golden years without undue financial stress.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/understanding-and-navigating-credit-scores-during-your-golden-years-a-guide-for-retirees.html