As we approach the end of the second quarter, we find ourselves propelled by a whirlwind of anticipation about late window dressing. Reflecting on the past three months, the theme that most readily comes to mind is “AI Mania.” However, it is certainly more than that.

Indeed, it would be easy to observe the 12+% gain for the NASDAQ 100 (NDX), credit the market-leading mega-cap techs, and conclude our analysis there. But such a view would be oversimplified. The S&P 500 Index’s impressive rise of over 8% this quarter, while largely bolstered by the mega-cap technology companies, also has other contributing factors.

We’ve started to see early signs of market rotation, with other sectors beginning to participate in the rally. The Russell 2000’s quarter-to-date gains are nudging towards 5%. European stocks, after posting double-digit gains in the first quarter, are only modestly higher on balance. Japan’s Nikkei 225 index, boasting a remarkable 20% gain, has been a standout. Conversely, China’s reopening didn’t quite match the initial enthusiasm, with both Mainland Chinese and Hong Kong indices declining.

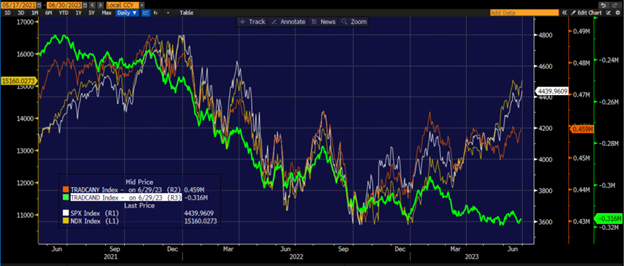

However, the market rotation is far from over. The chart below shows that while advance/decline lines have shown some recovery, they are yet to fully confirm the recent market movements:

1-Year Line Chart, SPX (white), NDX (yellow), NYSE Cumulative Advances-Declines (red), NASDAQ Cumulative Advances-Declines (green)

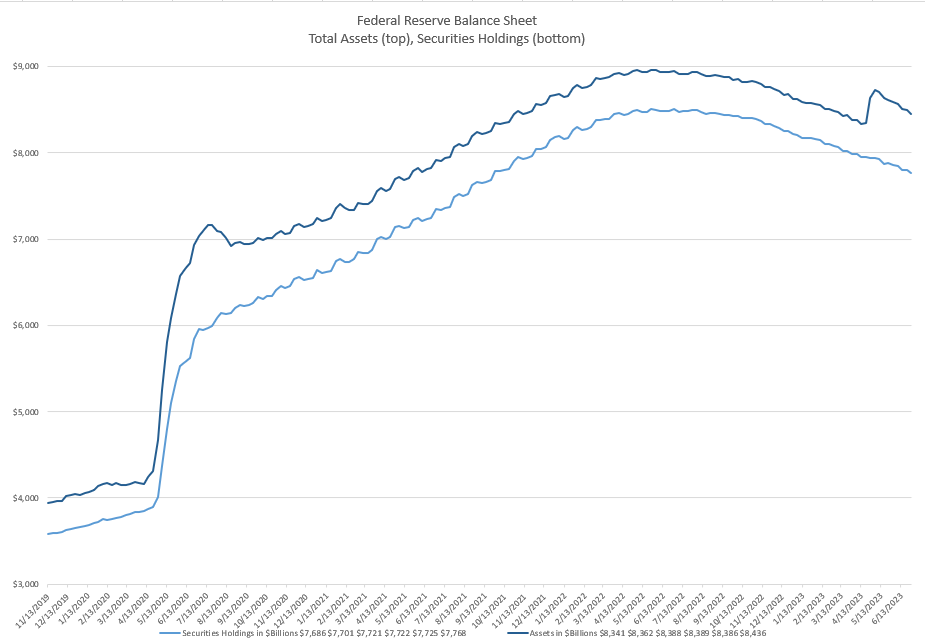

Interestingly, the banking crises that peaked last quarter seem to have served as a primary catalyst for this quarter’s run, especially in the U.S. While it may be tempting to simply say that “whatever doesn’t kill you makes you stronger,” it isn’t enough in this case. A key driver was the fact that the Federal Reserve’s balance sheet expanded by approximately $300 billion due to loans to the banking sector.

As we’ve noted before, the transmission of monetary policy displays a massive asymmetry. While rate hikes and quantitative tightening (QT) have a long and variable lag, markets react within weeks to any form of monetary accommodation. Even though the accommodation wasn’t specifically targeted at markets, the balance sheet expansion quickly reached already buoyant markets. The abrupt reversal of several months’ worth of QT evidently provided a shot of adrenaline to markets primed for action. Even though QT has now returned the balance sheet to previous levels, equity market enthusiasm persists, even if it has lost momentum in the bond market.

Looking forward, equities are expected to face a rigorous examination when the second-quarter earnings season kicks off in about two weeks. Much of the current rally, particularly in the tech sector, has occurred in the form of multiple expansion. In other words, in the equation for P/E ratios, the ‘P’ (price) has been outpacing the ‘E’ (earnings). Implicitly, it means that earnings expectations have risen, regardless of whether the published estimates reflect them. One key factor driving this quarter’s rally was a strong response to first-quarter earnings in April. Most companies met or modestly beat expectations, with some, like Nvidia (NVDA), soaring on positive guidance. However, we must question whether the bar has been set too high, at least in the short term.

On that note, I was recently asked whether investors should take profits after the remarkable rally and ahead of earnings season. My suggestion? Opt for insurance instead. With the VIX hovering around 13, volatility is at its lowest levels since February 2020. Given that the VIX is intended to offer the market’s best estimate of volatility over the coming 30 days, which will encompass the core of earnings season, volatility traders appear quite placid. Volatility protection can be compared to insurance: you don’t necessarily want it to pay off, but it can provide peace of mind. As the value of the assets it’s designed to protect has appreciated over time, opting for this insurance when it’s cheap could prove to be a wise move.

In conclusion, as we look back on the second quarter of 2023, the key themes that emerge are AI Mania, the start of a market rotation, and the ongoing impact of monetary policy. As we move forward, these themes will continue to inform and shape the investment landscape. Understanding them is crucial to navigating the challenges and opportunities that lie ahead.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/the-second-quarter-synopsis-ai-mania-market-rotations-and-monetary-policy-dynamics.html