Introduction:

As the year draws to a close, savvy investors are exploring strategies to optimize their tax liabilities and preserve more of their hard-earned money. One often-overlooked yet potent technique is tax-loss harvesting. This proactive strategy involves turning investment losses into a tax advantage by strategically selling underperforming assets. In this comprehensive guide, we’ll delve into the intricacies of tax-loss harvesting, its potential benefits, and actionable steps you can take before the December 31 deadline.

Understanding Tax-Loss Harvesting: A Path to Tax Efficiency

Tax-loss harvesting is not merely a reactive measure to mitigate losses but a proactive strategy with the potential to reduce current and future tax burdens. By strategically selling investments that are in the red, investors can replace them with similar assets, offset realized gains, and ultimately redirect more money back into their portfolios.

The Two-Fold Impact: Current Gains and Future Deductions

Tax-loss harvesting offers a dual benefit by addressing both current gains and future income. The losses incurred can be used to offset realized investment gains, providing immediate relief on taxable income. Moreover, any remaining losses, up to $3,000 ($1,500 for married individuals filing separately), can be applied against ordinary income on your tax return, effectively reducing your overall tax liability.

Christopher Fuse, Asset Allocation Portfolio Manager at Fidelity, emphasizes the potential of tax-loss harvesting in volatile markets, describing it as an episodic opportunity that can insulate taxable gains for several years.

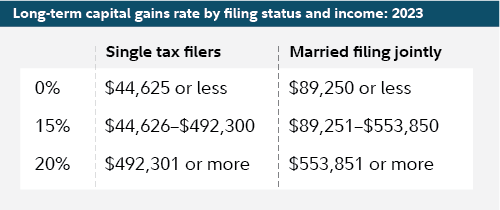

Short-Term vs. Long-Term Gains and Losses

Understanding the tax implications of short-term and long-term gains and losses is crucial to maximizing the benefits of tax-loss harvesting. Short-term capital gains, realized from investments held for one year or less, are taxed at ordinary income rates, potentially reaching as high as 40.8% for high earners when factoring in the net investment income tax (NIIT) and state/local taxes. In contrast, long-term capital gains enjoy a significantly lower tax rate, with a maximum of 23.8% for high earners.

Gains and Losses in Mutual Funds

For mutual fund investors, gains and losses often come in the form of distributions. Short-term capital gains distributions from mutual funds are treated as ordinary income, limiting the offsetting possibilities with capital losses. Tax-loss harvesting becomes especially relevant for managing these distributions and optimizing tax savings.

Harvesting Losses for Maximum Tax Savings

When implementing tax-loss harvesting, focusing on short-term losses provides the greatest benefit, as they can offset short-term gains taxed at higher rates. Fuse recommends identifying investments that no longer align with your strategy or have poor growth prospects. Harvesting short-term losses first allows for more effective tax planning.

Moreover, realizing capital losses, even without corresponding gains in the current year, can still be beneficial. The tax code permits applying up to $3,000 a year in remaining capital losses to offset ordinary income, with any excess losses carried forward for future use.

Staying Diversified and Avoiding Wash Sales

Careful consideration must be given to maintaining a diversified portfolio while avoiding wash sales, which can negate the tax benefits of harvesting losses. The wash-sale rule disallows tax write-offs if the same or substantially identical securities are repurchased within 30 days before or after selling loss-generating investments.

To stay diversified without triggering wash-sale rules, consider substituting a mutual fund or ETF targeting the same industry instead of repurchasing identical securities. Investors should consult a tax advisor to ensure compliance, especially if dealing with stock bonuses or employee stock purchase plans.

Integrating Tax-Loss Harvesting into Year-Round Strategies

To maximize the value of tax-loss harvesting, consider integrating it into your year-round tax planning and investing strategy. Professional portfolio managers, like Fuse, design portfolios with tax efficiency in mind, allowing for effective tax-loss harvesting as market dynamics evolve.

Fuse also emphasizes the synergy between tax-loss harvesting and portfolio rebalancing, providing an opportunity to reassess lagging investments ripe for harvesting. For individuals receiving stock bonuses, strategic tax-loss harvesting can prevent an unintended concentration of company stock in their portfolios.

Selecting the Most Advantageous Cost Basis Method

The method used to calculate the cost basis of investments can impact the effectiveness of tax-loss harvesting. Choosing the actual-cost method enables investors to designate specific, higher-cost shares for sale, maximizing the realized loss.

Balancing Tax Optimization and Investment Goals

While tax savings are crucial, it’s essential not to let the tax tail wag the investment dog. Implementing tax-loss harvesting should align with your overarching investment goals. A balanced strategy that prioritizes portfolio growth and risk management remains paramount.

Conclusion: A Strategic Approach to Tax Efficiency

As the year-end approaches, investors have a valuable window of opportunity to leverage tax-loss harvesting for immediate and future tax benefits. By understanding the nuances of this strategy, staying informed about tax implications, and consulting with tax professionals, investors can proactively manage their tax liabilities. Tax-loss harvesting isn’t just a year-end task—it’s a powerful year-round tool for maximizing tax efficiency and ensuring your investments work harder for you. Act before December 31 to seize the full potential of tax-loss harvesting and pave the way for a more tax-efficient financial future.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/strategic-tax-loss-harvesting-a-powerful-tool-to-slash-capital-gains-taxes-on-investments.html