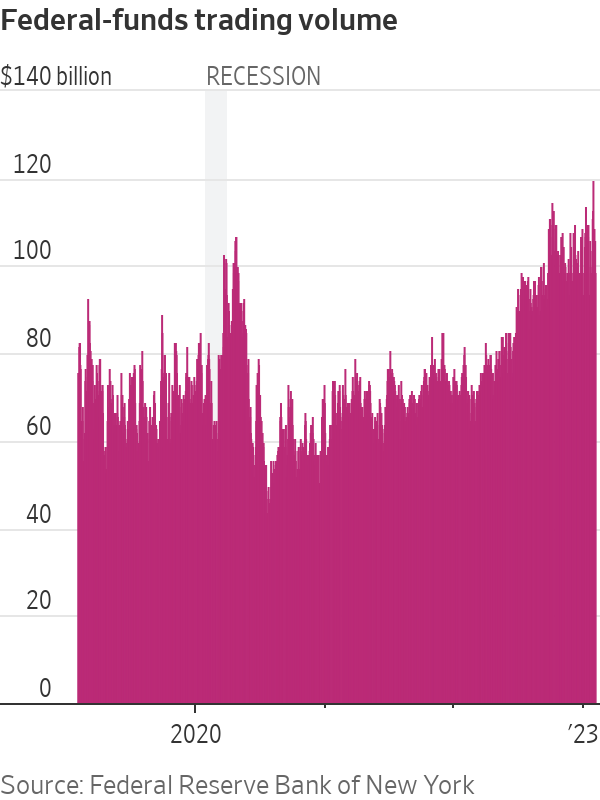

During the height of the pandemic, banks were facing a withdrawal of deposits. Currently, some financial institutions are offering higher interest rates to maintain their cash flow. On January 27th, borrowing in the federal-funds market reached $120 billion, the highest amount recorded in Federal Reserve data since 2016. The central bank’s recent hike in interest rates has caused a surge in activity in the fed funds market, which is utilized by banks and government-backed lenders to exchange their cash reserves held at the Fed.

Certain banks are in a rush to borrow funds, as they strive to improve their liquidity and comply with regulatory mandates while their customers seek higher-yielding investment products. Typically, fed-funds trades involve an overnight loan from a Federal Home Loan Bank to a commercial bank. Since the government-sponsored entities cannot earn interest by keeping their funds at the Fed, they lend their excess cash to banks without the need for securities to back the loan.

The identity of the banks involved remains confidential. In the past, most borrowers were foreign banks seeking to profit from borrowing cheaply in fed funds and then depositing the funds at the Fed to earn more interest. However, Bank of America reports that an increasing number of US banks are participating in the market, possibly because borrowing in fed funds is viewed favorably by regulators.

The aggressive bidding by some commercial banks has inflated the cost of fed-funds transactions, according to New York Fed data. The highest borrowing rates are now 0.15 percentage points above the Fed’s target range of 4.5% to 4.75%, and more than 0.3 percentage points above the median or effective fed-funds rate. Until October, all trades were priced below the target range, and no portion had exceeded it since March 2020.

The fed-funds rate serves as a benchmark for borrowing costs across the economy. The Fed sets a target range for the rate, but daily trading determines the actual rate. A substantial decrease in liquidity could result in a surge in the rate, putting stress on the ability of banks and companies to finance their operations.

“Banks prefer to avoid competition for funding,” says Mark Cabana, Head of US Rates Strategy at Bank of America Global Research. “However, the Fed aims to tighten financial conditions, and borrowing in the fed-funds market is one way to achieve this goal.”

According to Federal Deposit Insurance Corp data, U.S. banks experienced a record-breaking decline in deposits during the second and third quarters of 2022. During the third quarter, deposits fell by $206 billion to $19.357 trillion, extending the decline from the previous quarter of $370 billion. This marked the first consecutive quarter decline since 2010.

Community banks are facing significant challenges in keeping up with the higher interest rates offered by Treasurys and money-market funds, resulting in a loss of customers to these products. To secure cash on their balance sheets, many lenders have resorted to tapping FHLB advances, long-term borrowings backed by high-quality securities, and, to a lesser extent, the Fed’s discount window.

Blake Gwinn, the head of U.S. rates strategy at RBC Capital Markets, mentions that the increase in fed-funds borrowing may be due to home-loan banks keeping cash readily available in case of member advances. Additionally, as banks demand longer-term loans at the highest rate since early 2020, FHLBs would rather keep their cash invested in daily products instead of locking it up in less accessible securities.

Although some banks are paying a premium for funding, Gwinn states that “we are not seeing flashing red lights that things are getting tight.”

The liquidity-coverage ratios of Canada’s five largest banks, among the largest foreign banks, are at pre-pandemic levels, able to handle potential bank runs. A recent European Banking Authority study showed that as of June 2022, none of the hundreds of banks on the continent had failed to meet regulators’ liquidity measures, even after a notable decline in deposits and liquidity in the first half of 2022. The study found that the average bank was more than capable of withstanding potential turmoil.

As recently as last year, banks were inundated with depositors, and one solution was to steer clients towards money-market funds. Now, banks are competing with these funds for customers’ business.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/record-decline-in-u-s-bank-deposits-amid-competition-with-treasurys-and-money-market-funds.html