The recent news from across the Atlantic took the global financial community by surprise when French President Emmanuel Macron took the audacious step of raising the legal retirement age in his country from 62 to 64. This bold move, bypassing parliament, sparked significant controversy and could potentially provoke a vote of no confidence against his government.

According to President Macron, the unpopular pension reform is a necessary measure to address financial deficits stemming from pandemic spending and the ongoing European energy crisis. The world, and particularly the U.S., watches these developments closely, prompting questions about whether France’s pension reform could become a model for future changes to Social Security.

The French case is particularly intriguing as the country boasts one of the most generous pension systems in the European Union (EU). According to 2020 data, France allocated a staggering 14.7% of its GDP to pensions alone. However, the sustainability of such a system is currently under threat due to demographic shifts.

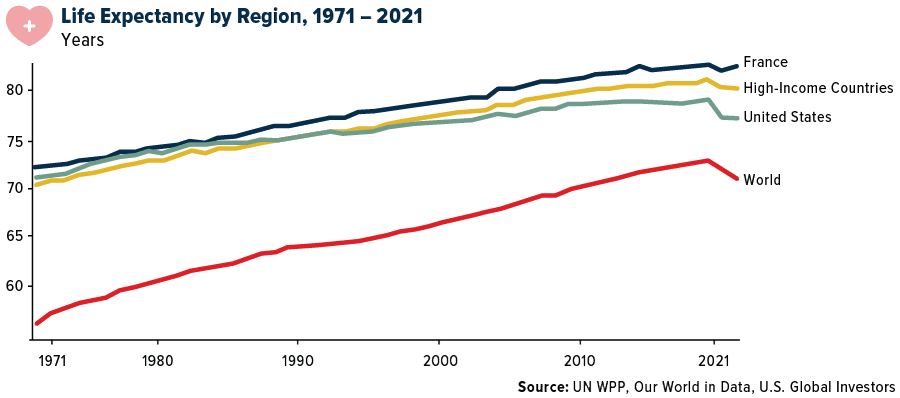

France has one of the highest life expectancies globally, and the expected years in retirement have significantly increased. As per the Organization for Economic Cooperation and Development (OECD), French men are expected to spend 23.5 years in retirement on average, second only to men in Luxembourg. The number climbs even higher for women, to 27.1 years.

Simultaneously, like other high-income countries, especially in Europe, France’s birth rate has been on a steady decline. Fewer workers to support a rapidly aging population is a stark reality that cannot be ignored. The statistics speak for themselves – in 2021, there were 10.5 births in France per 1,000 people, a notable decrease from 13.2 births 30 years earlier.

Could The U.S. Be Next?

The U.S. is indeed keenly observing the political repercussions of France’s retirement reform. If the widespread strikes and marches are any indication, the Macron government’s future appears unstable.

However, the truth is that the U.S. might be heading towards a similar crossroads. As of now, Sixty-six million Americans rely on monthly benefits from Social Security, a system projected to be insolvent by 2035 if current conditions persist.

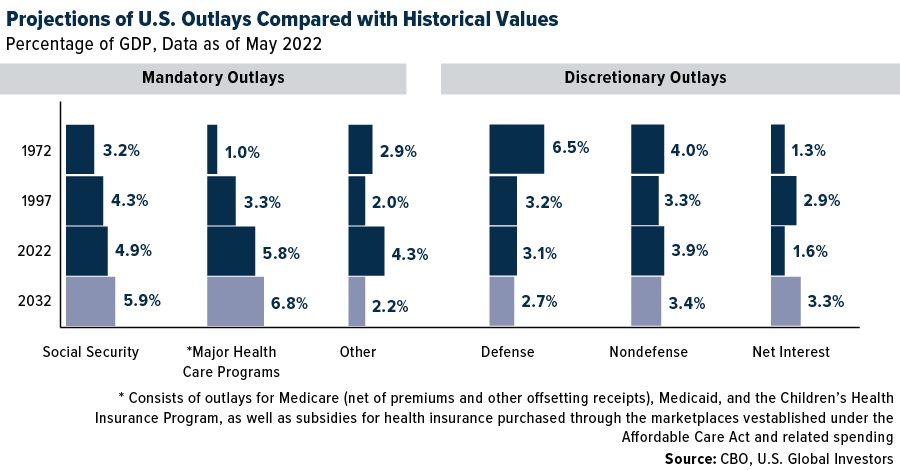

The Congressional Budget Office’s (CBO) projections show that by 2032, Social Security will account for nearly 6% of U.S. GDP, a noticeable increase from approximately 5% today. Major healthcare programs like Medicare and Medicaid are expected to consume an even more significant portion of the economy as older Americans continue to constitute a larger share of the total population.

Several potential reforms are under consideration, including raising the retirement age to as high as 70 and increasing the amount of annual wages subject to the Social Security payroll tax. Another option on the table is privatization, which carries inherent investment risks, as illustrated by the 19% loss recorded by corporate retirement plans in the U.S. in 2022.

What Does This Mean For American Savers?

The takeaway for Americans is clear – relying on Social Security in its current form for retirement is a risky gamble. Now more than ever, it’s critical for Americans to take charge of their own retirement planning.

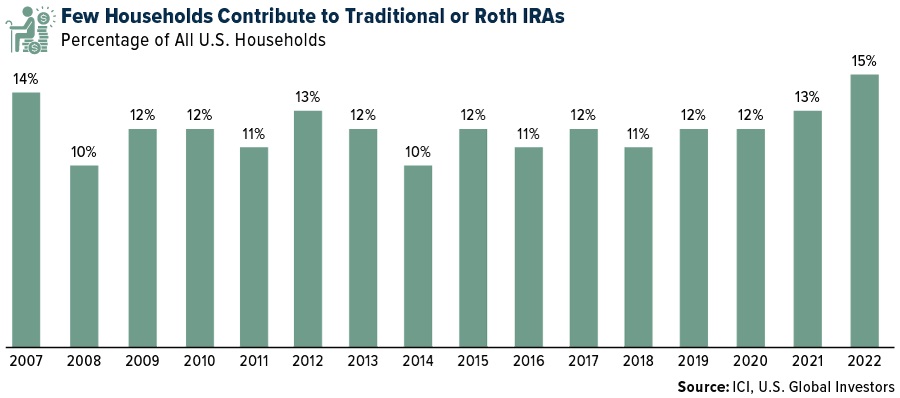

However, this might be easier said than done. In a surprising statistic revealed by the Investment Company Institute (ICI), only a paltry 15% of American households contributed to a traditional or Roth IRA in 2022. The more worrying number is that a significant 59% of households don’t own an IRA at all.

Taking a proactive approach to retirement planning can better equip Americans for a financially secure future. This strategy minimizes dependence on Social Security and mitigates potential risks associated with system changes.

To facilitate this, we’ve created the ABC Investment Plan. This initiative is aimed at guiding those unsure of where to begin their financial planning journey. With a modest initial investment and an affordable monthly contribution, you can start investing in our funds. The ABC Investment Plan is a systematic investment plan that leverages the benefits of dollar-cost averaging—a technique allowing you to invest a fixed amount in a specific investment at regular intervals. This, combined with financial discipline, can assist you in working towards your financial objectives.

As the French example underlines, change is often inevitable. Faced with shifting demographics and economic uncertainty, governments worldwide, including the U.S., may have to make tough decisions about their retirement systems. By taking control of your retirement planning now, you can better safeguard your future and potentially enjoy a more comfortable and secure retirement.

Let’s not forget the key lesson here: proactivity. Waiting on the sidelines hoping for Social Security to solve all retirement issues is a risky strategy. Instead, a proactive and informed approach towards retirement planning can significantly contribute to financial independence and security in your golden years.

It’s time for all of us to learn from the French example and understand that our retirement’s financial health is ultimately in our own hands. We must take control of our financial futures and start investing today for a comfortable retirement tomorrow. The ABC Investment Plan offers a simple, effective, and disciplined approach towards achieving this goal.

In conclusion, while we watch the developments in France and potentially brace for similar changes in the U.S., it’s essential to remember that every challenge presents an opportunity. The current situation is a powerful reminder for us to take control of our retirement planning and look beyond Social Security for financial security in our retirement years. By doing so, we not only contribute to our own financial wellbeing but also play a part in reducing the burden on national social security systems. It’s time to plan, invest, and secure our future.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/navigating-retirement-reforms-lessons-from-france-and-implications-for-the-u-s-social-security-system.html