By Ashlea Ebeling

Navigating the complex world of estate planning has become increasingly challenging for older Americans hoping to bequeath their retirement savings to their grandchildren without leaving them a substantial tax bill. Recent changes to estate planning rules have greatly influenced how heirs must handle inherited retirement accounts, requiring most non-spouse beneficiaries to withdraw these funds within ten years instead of the previously allowed several decades.

The shift in the rules has seen a trend of grandparents reassessing their estate plans, creating new trusts and strategies to maximize their family’s after-tax wealth. Some are also making proactive moves, like conducting Roth conversions or making substantial generation-skipping lifetime gifts.

With Americans holding a staggering $12.5 trillion in IRAs as of the end of March 2023, the potential tax implications for beneficiaries are significant. In fact, over half of households led by someone aged 65 or older have an IRA according to the Investment Company Institute, making it vital to plan ahead.

Let’s take a look at the approach of Linda O’Brien, an 83-year-old widow from Old Tappan, N.J. To bypass potential tax hurdles for her heirs, she decided to convert her traditional IRA into a Roth IRA, allowing her children and grandchildren to inherit the money tax-free. The money now grows tax-free in the Roth, and upon inheriting it, her grandchildren can withdraw it tax-free. She essentially prepaid the taxes, a strategic move that others may consider.

Under the old rules, naming grandchildren as beneficiaries on individual retirement accounts was a popular move. Young heirs could stretch out annual required minimum distributions over their lifetime, but the 10-year window changed the equation. Now, inherited IRAs can generate large tax bills, particularly if distributions coincide with the grandchildren’s or their parents’ peak earning years. Minors may even need to file a tax return to report the IRA payouts, which could be taxed at their parents’ rate.

Despite this, leaving a Roth IRA can help circumvent some issues associated with the accelerated tax hit from an inherited traditional IRA. Grandparents can move money from a traditional IRA to a Roth, paying income taxes on the transfer.

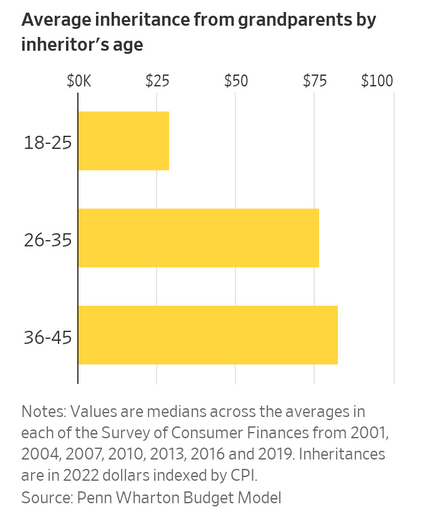

While the chances of receiving an inheritance from a grandparent are low, those fortunate enough to do typically receive a substantial sum. Jon Huntley, a senior economist at the Penn Wharton Budget Model, found that between 2001 and 2019, those aged 18 to 25 had a 2% chance of inheriting from a grandparent over five years, with the average inheritance amounting to $29,000.

Here are some key points to consider when planning your legacy to your grandchildren:

Generational Skipping:

It’s not unusual for grandparents to begin gifting their grandchildren soon after their birth, from buying diapers and paying for preschool to establishing college 529 savings plans and special trusts. This strategy not only provides immediate support but can also be a smart tax move.

An important part of estate planning is deciding when and how much you want your heirs to benefit and how you want to control the funds’ usage.

Caroline McKay, a senior wealth strategist at CIBC Private Wealth in Boston, cautions that leaving an IRA outright to grandchildren, even with a 10-year payout period, could lead to irresponsible spending. Having open discussions about your intentions for the money—like a house down payment or starting a business—increases the likelihood that your grandchildren will honor your wishes.

Administrative Challenges:

Inherited IRAs come with complications beyond just payouts. For instance, you cannot convert an inherited traditional IRA into a Roth, add money to an inherited IRA, or combine it with your own IRA.

IRA custodians such as Schwab and Vanguard facilitate the establishment of a minor’s inherited IRA with a designated adult to manage the account until the minor reaches the age of majority. However, in certain cases, court-appointed guardians may be required.

When to Utilize Trusts:

Trusts can complicate the estate planning process, but they provide a valuable mechanism for controlling how your inheritance is used. If you have concerns about how your grandchildren or their partners might manage the inheritance, a trust can offer a solution. A trustee will distribute the money based on your predetermined conditions, offering you peace of mind about the future use of your assets.

Take, for example, the case of Ralph and Cindy Dorio. They wanted their 20-year-old granddaughter to inherit her deceased mother’s share of their estate, including their IRAs. However, they opted to leave her inheritance in a trust managed by her uncle to prevent the young heir from potential financial mismanagement.

In conclusion, while it may feel daunting to navigate the changing landscape of estate planning and retirement savings, there are effective ways to pass down wealth to your grandchildren without the associated tax burden. The key is to remain proactive, consider employing strategic mechanisms like Roth conversions and trusts, and always communicate openly with your beneficiaries about your intentions.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/leaving-a-lasting-legacy-without-the-tax-burden-a-comprehensive-guide-for-grandparents.html