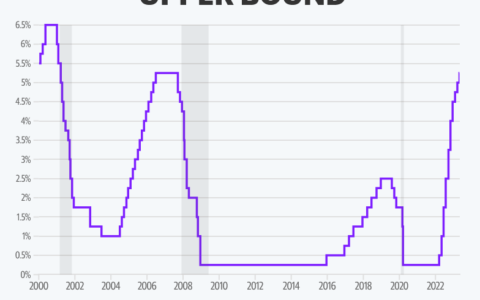

The Federal Reserve recently made headlines with a significant move, cutting its key interest rate by 0.50 percentage points, bringing the federal funds rate to a target range of 4.75% to 5.00%. This decision was anticipated by many investors, though there was some speculation as to whether the Fed would opt for a more moderate 0.25% cut or take the bolder step of a 0.50% reduction. Now that the rate cut is official, what does it mean for the economy, consumers, and investors?

Let’s dive into six key takeaways that shed light on the reasons behind the Fed’s decision and the impact it will have.

1. What Has Changed Since the Last Fed Meeting?

The Federal Reserve has two main objectives, often referred to as its “dual mandate”: keeping inflation low and stable, and maintaining low unemployment. For much of the past few years, the Fed has primarily focused on inflation, as it skyrocketed during the post-pandemic recovery. However, the economic landscape has shifted recently.

The latest data shows that inflation has been gradually decreasing. Both the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) Price Index, which are key measures of inflation, now hover around 2.5%—much closer to the Fed’s 2% target. With inflation easing, the Fed has turned its attention more toward unemployment, which has been creeping up. Unemployment, once as low as 3.4% earlier in 2023, has now risen to 4.2%.

This uptick in unemployment, coupled with revised data showing fewer jobs created earlier in the year than initially thought, is a clear sign that the labor market is cooling. As a result, the Fed has shifted its focus to balance both inflation and employment, and the rate cut reflects that pivot.

2. Does the Rate Cut Suggest the Economy Is in Trouble?

At first glance, a stronger focus on unemployment might seem concerning. However, it’s important to put things into perspective. While the labor market is cooling, this is largely a correction from the unusually hot levels seen in the wake of the pandemic. The US economy, according to the Federal Reserve’s Asset Allocation Research Team (AART), is still in an expansion phase, and the current job market is healthy by historical standards.

Fed Chair Jerome Powell has acknowledged the cooling labor market but emphasized that the Fed is not comfortable with further increases in unemployment. This rate cut is part of an effort to provide some support to the economy while inflation remains under control.

3. Why Did the Fed Opt for a 0.50% Cut?

Investors were expecting a rate cut, but there was debate about the size—0.25% or 0.50%. The Fed’s decision to go with the larger cut may reflect a strategy of “front-loading” rate cuts. The central bank knows that monetary policy impacts the economy with a lag, meaning it can take months for the effects of a rate change to filter through to the broader economy.

By starting with a more significant cut, the Fed is signaling its intention to move swiftly in response to changing economic conditions. Additionally, the current federal funds rate remains above what many economists consider the “neutral” policy rate, which is estimated to be around 4%. A neutral rate is one that neither stimulates nor restricts economic growth. By cutting the rate more substantially, the Fed is effectively taking its foot off the economic brakes, allowing for a more accommodating monetary policy.

4. Is the Timing of This Cut Politically Motivated?

Some might speculate that the timing of the rate cut is linked to the upcoming November elections, as this was the last chance for the Fed to adjust rates before Election Day. However, Fed Chair Powell has consistently maintained that the Federal Reserve remains independent of political considerations.

“We never use our tools to support or oppose a political party, a politician, or any political outcome,” Powell said at a press conference following the FOMC’s July meeting. The data, not politics, has driven this decision. With inflation easing and unemployment rising, the conditions were right for a rate cut, regardless of the election calendar.

5. How Soon Will More Rate Cuts Follow?

Following this rate cut, the Federal Reserve provided an updated set of economic projections, including the widely-watched dot plot—a chart showing the expected path of interest rates over the coming years based on Fed members’ views. According to this updated dot plot, the median expectation among Fed members is that the federal funds rate will fall to a range of 4.25% to 4.50% by the end of 2024. This implies the potential for two more rate cuts of 0.25% in the remaining meetings of this year.

However, it’s important to note that these projections are not set in stone. The Fed has repeatedly emphasized its “data-dependent” approach, meaning that future rate cuts will be influenced by how economic data evolves, particularly in relation to inflation and the labor market. Investors should watch closely for trends in jobless claims and hiring, as these will play a crucial role in shaping future Fed policy.

Longer-term, interest rates may not fall as low as some investors hope. Fidelity’s AART suggests that inflation could remain slightly above the Fed’s 2% target, possibly around 3%, which could limit how much further rates are reduced in the future.

6. What Do Rate Cuts Mean for Consumers and Investors?

The Federal Reserve controls short-term interest rates, but its decisions have ripple effects throughout the financial markets. For consumers, lower interest rates typically translate to reduced borrowing costs. This is especially relevant for debt tied to the prime rate, such as credit card balances and variable-rate loans. Homebuyers and homeowners with variable-rate mortgages may also see some relief as rates begin to decline.

For savers, lower interest rates may lead to lower yields on savings accounts, money market funds, and short-term CDs. However, it’s important to note that the bond market often reacts to rate cuts before the Fed officially lowers rates. As a result, yields on longer-term debt like 10-year Treasurys and 30-year mortgages have already been falling in anticipation of rate cuts.

Investors should pay attention to how lower rates impact different asset classes. In the short term, falling rates often provide a boost to the stock market, as borrowing costs decline and consumer spending increases. Bonds, particularly those with longer maturities, may also see price increases as yields fall. However, the lower yields could make bonds less attractive to income-seeking investors over time.

Conclusion

The Federal Reserve’s decision to cut interest rates marks a pivotal moment for the US economy. While inflation continues to moderate, the Fed is increasingly focused on ensuring that unemployment remains under control. By opting for a larger-than-expected rate cut, the Fed has signaled its intention to act swiftly in response to a cooling labor market. For consumers and investors, these changes will have important implications, from borrowing costs to investment strategies. As always, staying informed and being prepared to adjust your financial plans is key to navigating these evolving economic conditions.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/interest-rates-are-finally-falling-6-things-to-know-about-the-impact-of-the-feds-pivotal-decision.html