At the heart of most financial discussions these days, inflation is the recurring boogeyman that haunts the dreams of economists and investors. A core inflation rate below 3% would be a reason for the Federal Reserve to heave a sigh of relief, and it would have a positive domino effect on stocks, sparking an uptrend and quelling consumers’ anxieties about the escalating cost of living. But can this dream become reality? It seems possible, especially if we choose to measure U.S. price changes the way Europe does.

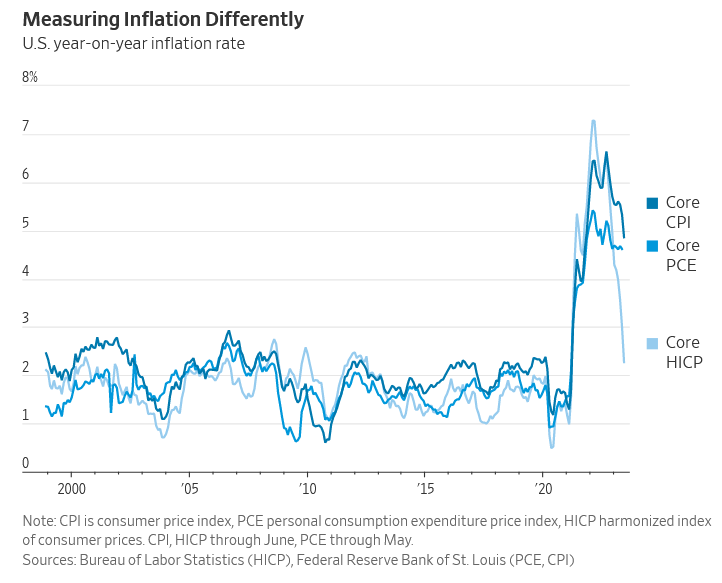

In May, by European standards, the U.S. had already dipped below the dreaded threshold, dropping even further in June. However, a stark contrast is painted when U.S. inflation data is measured the traditional way; the figures announced last Wednesday showed core inflation reaching a significant 4.8% for June. This discrepancy stems from the different methodologies employed by the U.S. and Europe in calculating inflation. The U.S. Bureau of Labor Statistics (BLS) does calculate American price increases the European way, though this alternative is relatively less known.

It is indeed baffling to see such a radical discrepancy between the two methods, enough to throw off investors who might be inclined to believe the current consensus: that inflation is decreasing, though not as rapidly as the Fed would prefer. The alternative narrative suggested by the lower European figures may disrupt this perceived stability.

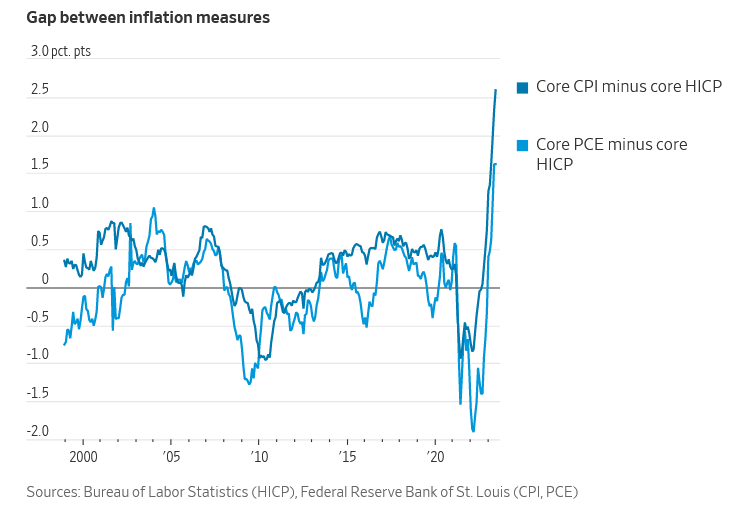

The difference primarily arises from what each measure excludes. The U.S. core inflation, which eliminates the volatile factors of food and energy, was measured at 2.6 percentage points higher than the European-style inflation, otherwise known as the Harmonized Index of Consumer Prices (HICP). This marked the greatest gap ever recorded between these two measures. The HICP excludes what is called “owners’ equivalent rent” or imputed rent, an imaginary cost that a homeowner would pay to rent their own home, which makes up about a third of the U.S. core CPI.

Removing such a contentious component, which is based on speculative calculations by homeowners on the rental value of their houses, can lower the core inflation to a more acceptable 2.3%. While it is important to consider food and oil prices due to their impact on the cost of living, their exclusion from core inflation allows a more focused view of whether the economy is generating pressures the central bank needs to mitigate.

So, why does inflation continue to be a cause for concern? The answer lies at the intersection of tradition, ignorance, and fear. The Consumer Price Index (CPI) has long been the preferred measure of inflation in the U.S., even though the Federal Reserve’s inflation target is based on the Personal Consumption Expenditures Price Index (PCE) from the Bureau of Economic Analysis. The PCE generally produces a lower figure than the CPI but still places considerable emphasis on imputed rent.

The Fed faces a challenge. Even if it were to regard the HICP as a superior measure—which it doesn’t appear to—there’s no easy path to making a change without political fallout. The inflation data is already subject to considerable scrutiny and skepticism from economists who argue that enhancements to the indexes typically result in lower inflation than previous methods.

The crux of these measurement dilemmas is determining if the economy’s underlying pressures are so robust that further restraint is necessary. If a vigorous jobs market leads to workers with larger paychecks, consumer demand could surge, allowing companies to increase prices. This scenario would compel the Fed to continue raising rates.

However, the lower core HICP inflation suggests that the robust jobs market may be less alarming than the CPI measure indicates. Hawks, however, worry that persistent above-inflation pay raises could fuel inflation, as companies pass on increased costs. This could potentially elevate inflation expectations, leading to further wage demands.

Conversely, if expensive borrowing causes companies to cut spending, hire fewer employees, and resist pay demands, wage growth could moderate and demand could decline, encouraging the Fed to relax its monetary policies—provided that the economic slowdown doesn’t turn into a recession.

While indicators often align after periods of divergence, the rent increases, which have slowed down, may cause the CPI and PCE to gravitate toward the HICP. Unfortunately, even if core inflation drops further, it will still exceed the comfort zone according to the CPI and PCE measures that the Fed and investors prioritize.

Inflation is not the sole economic indicator sending mixed signals. A multitude of indicators are telling different narratives about the state and direction of the economy, a topic I’ll revisit in the next installment of Streetwise. Meanwhile, the current inflation conundrum leaves me both concerned and confused—not an ideal state of mind when trying to predict market movements. Regardless, it’s important to remember that while the face of inflation may change depending on how we measure it, its impacts on our economy are real, persistent, and require informed interpretation and action.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/inflations-shapeshifter-measuring-it-the-european-way-and-seeing-beyond-the-hype.html