“How much do I need to retire?” This seemingly simple question is one that many grapple with as they approach retirement age. The answer is both complex and multifaceted, varying based on individual circumstances, desires, and uncertainties that loom large over future financial plans.

Decoding the Retirement Savings Factors

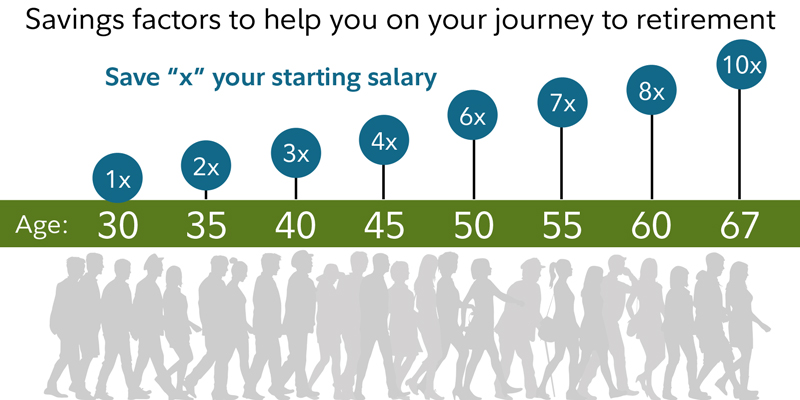

We dove deep into the data and have created a series of age-based retirement savings factors to serve as beacons in the often foggy landscape of retirement planning. It’s essential to note that while these milestones are aspirational, you may not hit every mark. However, they are valuable indicators and can guide you towards a comfortable retirement.

Here’s a basic structure based on our research:

- 15% Annual Savings from Age 25: This includes any employer matches.

- Invest Over 50% in Stocks: Historically, stocks have provided better long-term returns, so investing more than half of your savings in them can help you grow your nest egg over time.

- Retirement Age: We based our calculations on retiring at age 67, a common age for full Social Security benefits.

- Preretirement Lifestyle: Our factors are designed for those who wish to maintain their preretirement lifestyle during their retirement years.

Our research suggests that by the age of 67, aiming to save 10x your preretirement income should place you in a comfortable position. While this number may seem intimidating, remember that retirement planning is a marathon, not a sprint. Here are some goalposts:

- By 30: 1x your income

- By 40: 3x your income

- By 50: 6x your income

- By 60: 8x your income

Key Variables to Consider

Planned Retirement Age:

The age you retire significantly impacts your saving milestones. If you retire later, your savings have more time to grow, you’ll spend fewer years in retirement, and your Social Security benefits will be higher. For instance:

- Max, who wants to retire at 70, needs 8x his final income.

- Amy, aiming for 67, needs 10x.

- John, eyeing 65, requires a whopping 12x.

The takeaway here is clear: a longer career can lead to easier financial milestones for retirement.

Post-Retirement Lifestyle Expectations:

Your anticipated lifestyle can influence how much you need to save:

-

- Joe, who aims to downsize and live frugally, may only need 8x by 67.

- Elizabeth, aiming to maintain her current lifestyle, should save 10x.

- Sean, who dreams of extensive travel, should aim higher, at 12x.

What If I’m Falling Behind?

First, don’t panic. If you’re under 40, consider adjusting your portfolio to be more growth-oriented and increasing your savings rate. Understand the risks and rewards associated with different asset classes. If you’re over 40, a combination of increased savings, curbing unnecessary expenses, and potentially working a few more years can bridge the gap.

Conclusion: It’s Never Too Early (or Late) to Plan

If you’re not at your nearest milestone, don’t lose hope. The path to retirement is filled with twists and turns, but with diligence, planning, and adaptability, you can navigate your way to a comfortable retirement. The key is to take the initiative, understand your financial picture, and adjust when needed. Start now, and future you will surely be grateful.

Footnote: The specifics and examples provided in this article are hypothetical and for illustrative purposes. Everyone’s financial situation is unique, and it’s essential to consult with a financial advisor for personalized guidance.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/how-much-do-you-need-to-retire.html