When delving deep into the intricate world of economic data, employment reports are undeniably crucial. The Federal Reserve’s commitment to base its policy decisions on the “totality” of upcoming economic data underscores this importance. While we have a myriad of labor market indicators at our disposal, the monthly Employment Situation release holds a special place due to its comprehensiveness. Based on a careful evaluation of the most recent jobs figures, my analysis suggests a softening in labor market activity, rather than a weakening.

To understand the significance of these two seemingly similar terms, it’s vital to recognize that nuances matter, not just to economists or financial analysts but especially to major stakeholders like the Fed, money markets, and bond markets.

New Job Creation: An Essential Indicator

Undoubtedly, new job creation is the cornerstone of labor market health. The total nonfarm payrolls, which provide insights into the level of new jobs created, recorded an increase of +187,000 in August. At first glance, this surpasses expectations, particularly when considering that the economy has weathered 525 basis points in Fed rate hikes since the previous March.

However, it’s imperative not to let this singular data point overshadow the larger narrative. A crucial, albeit less-publicized detail, is the downward revision of the prior two months’ figures by a cumulative -110,000.

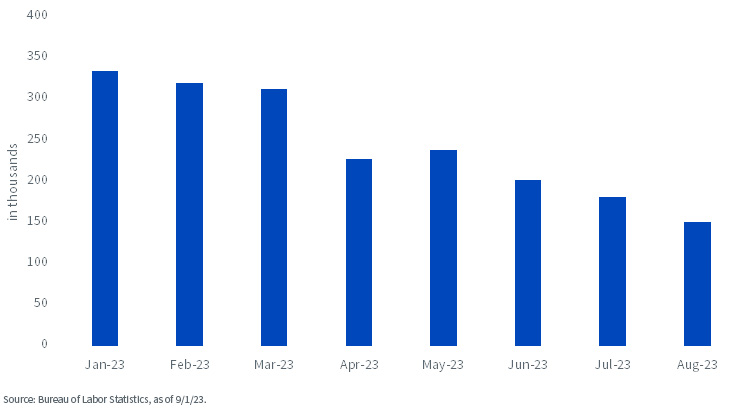

To mitigate the swings and vagaries of monthly data, I advocate for evaluating the three-month moving averages. It’s here that we observe a clearer trend of slowed new hiring, with the latest figures indicating a +150,000 new hire rate, a drop from July’s +181,000. The top bar chart confirms that this average has been on a gradual decline throughout the current year.

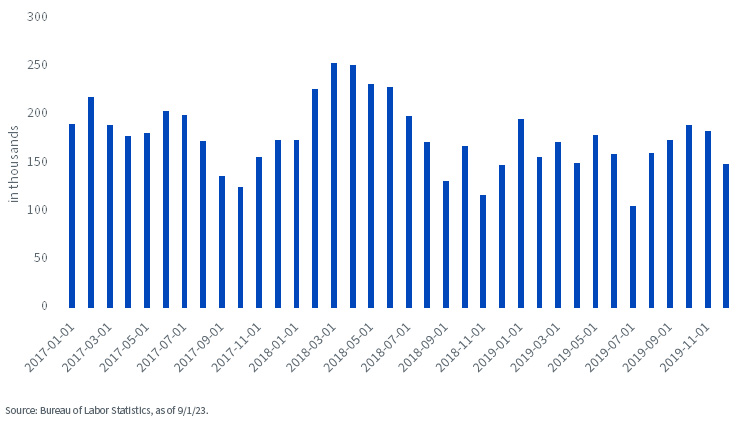

Yet, to offer a counter-perspective, drawing parallels with the three-year period from 2017 to 2019 (before the COVID-19 pandemic), the current levels of new job creation don’t seem bleak. In fact, they are only 27,000 shy of the average for that duration.

U.S. Total Nonfarm Payrolls – 3-Month Moving Average

Unemployment Rate: Beyond the Surface

Another vital metric that demands our attention is the unemployment rate. In August, there was a 0.3 pp rise, settling at 3.8%. However, delving deeper, the primary driver behind this was a considerable +736,000 increase in the civilian labor force – an indicator often hailed as a positive sign for labor market dynamics. Parallelly, civilian employment also witnessed a robust surge of +222,000. Unfortunately, this surge wasn’t sufficient to counterbalance the significant influx into the workforce.

Conclusion: What Lies Ahead?

The prevalent sentiment had been leaning against a Fed rate hike in the upcoming FOMC meeting. The employment data from August seems to align with this narrative. With one more CPI report to consider before the September 20th meeting, the overarching theme continues to be “higher for longer”. As of now, there’s no indication that rate cuts are on the immediate horizon, solidifying the Treasury market’s current posture.

In wrapping up, it’s paramount to differentiate between a market that’s slowing down and one that’s weakening. Current indicators suggest the former, implying a potential moderation, but not a downturn. As always, a nuanced understanding of economic indicators is key to informed policy and investment decisions.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/deciphering-the-u-s-labor-landscape-a-softened-pace-not-a-stumble.html