It’s easy to feel like everyone else has their financial act together—everyone, that is, except you. But the reality is that many people are anxious about their financial standing, particularly when it comes to retirement savings. If you’re wondering how you measure up, looking at average retirement savings by age can provide some useful insights. More importantly, knowing what steps to take to improve your savings rate can help you build a more secure future.

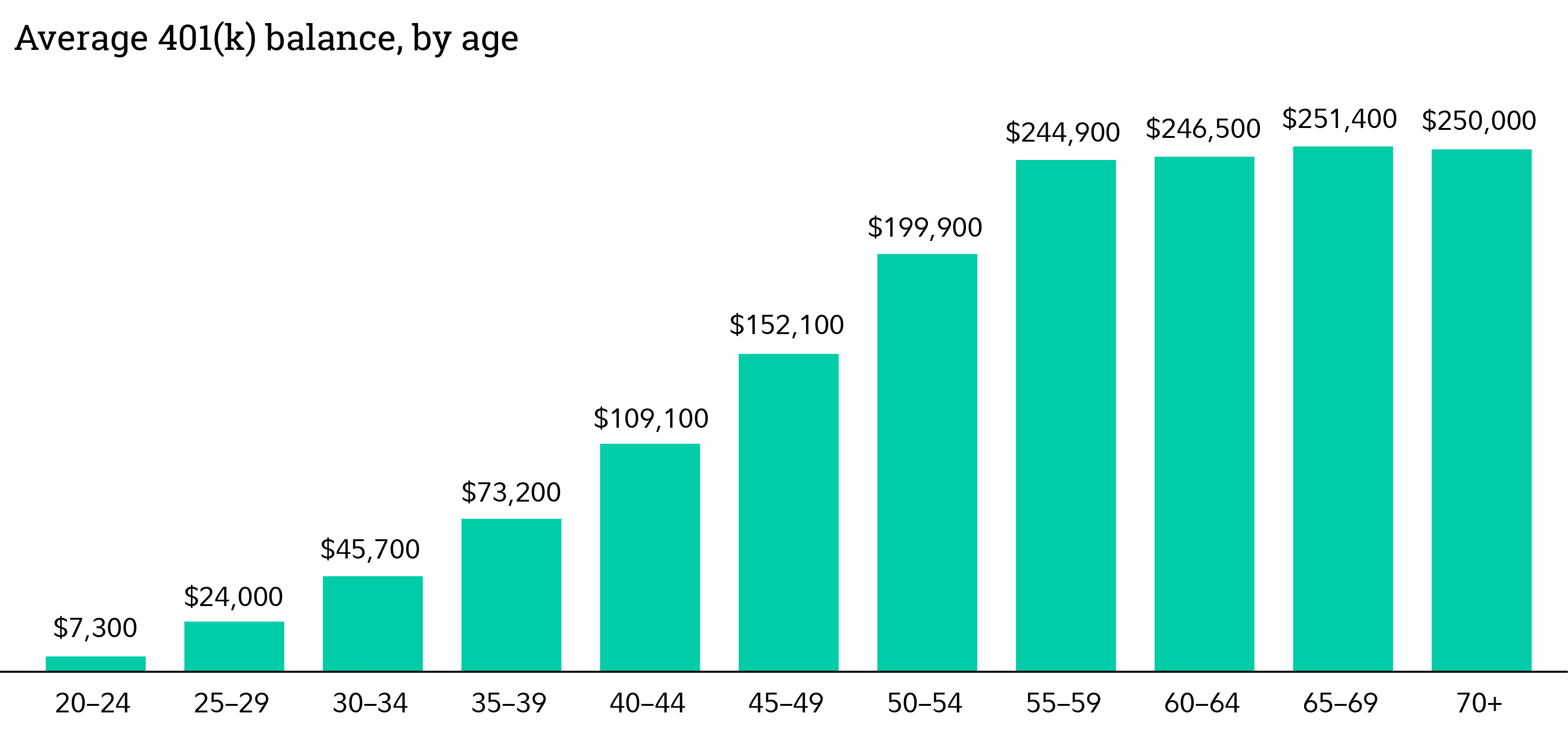

Average Retirement Savings by Age

Understanding how much others have saved at different stages of life can provide a useful benchmark. However, retirement savings vary widely because people often have money saved outside of traditional retirement accounts, such as real estate, brokerage accounts, and savings accounts. Still, looking at 401(k) and IRA balances offers a general sense of how prepared people are for retirement.

Retirement Savings by Generation

It’s no surprise that older generations have saved more for retirement than younger ones. Fidelity reports that the average savings rate across all age groups is 14.1%, which is close to the recommended 15% savings rate needed to maintain your lifestyle in retirement. This percentage includes both personal contributions and any employer-matching funds.

Here’s how retirement savings generally break down by generation:

- Gen Z (Early 20s): Just starting their careers, many are contributing to 401(k)s and IRAs, but their balances remain relatively low.

- Millennials (Mid-20s to Early 40s): Have started accumulating retirement funds but may still be behind due to student loans, home purchases, or other financial obligations.

- Gen X (Mid-40s to Late 50s): Approaching retirement age, this group should ideally have several times their annual salary saved.

- Baby Boomers (60s and beyond): Most are either already retired or making final contributions to their nest egg.

| Average 401(k) balance | Employee contribution | Employer contribution | Contributing to a Roth 401(k) | Investing 100% in target date fund | Loan outstanding | Average IRA balance | |

|---|---|---|---|---|---|---|---|

| Baby boomers | $249,300 | 11.9% | 5.0% | 12.2% | 44.2% | 14.5% | $257,002 |

| Gen X | $192,300 | 10.2% | 5.0% | 14.5% | 54.0% | 25.3% | $103,952 |

| Millennials | $67,300 | 8.7% | 4.6% | 18.3% | 70.1% | 18.4% | $25,109 |

| Gen Z | $13,500 | 7.2% | 3.7% | 18.2% | 81.5% | 6.7% | $6,672 |

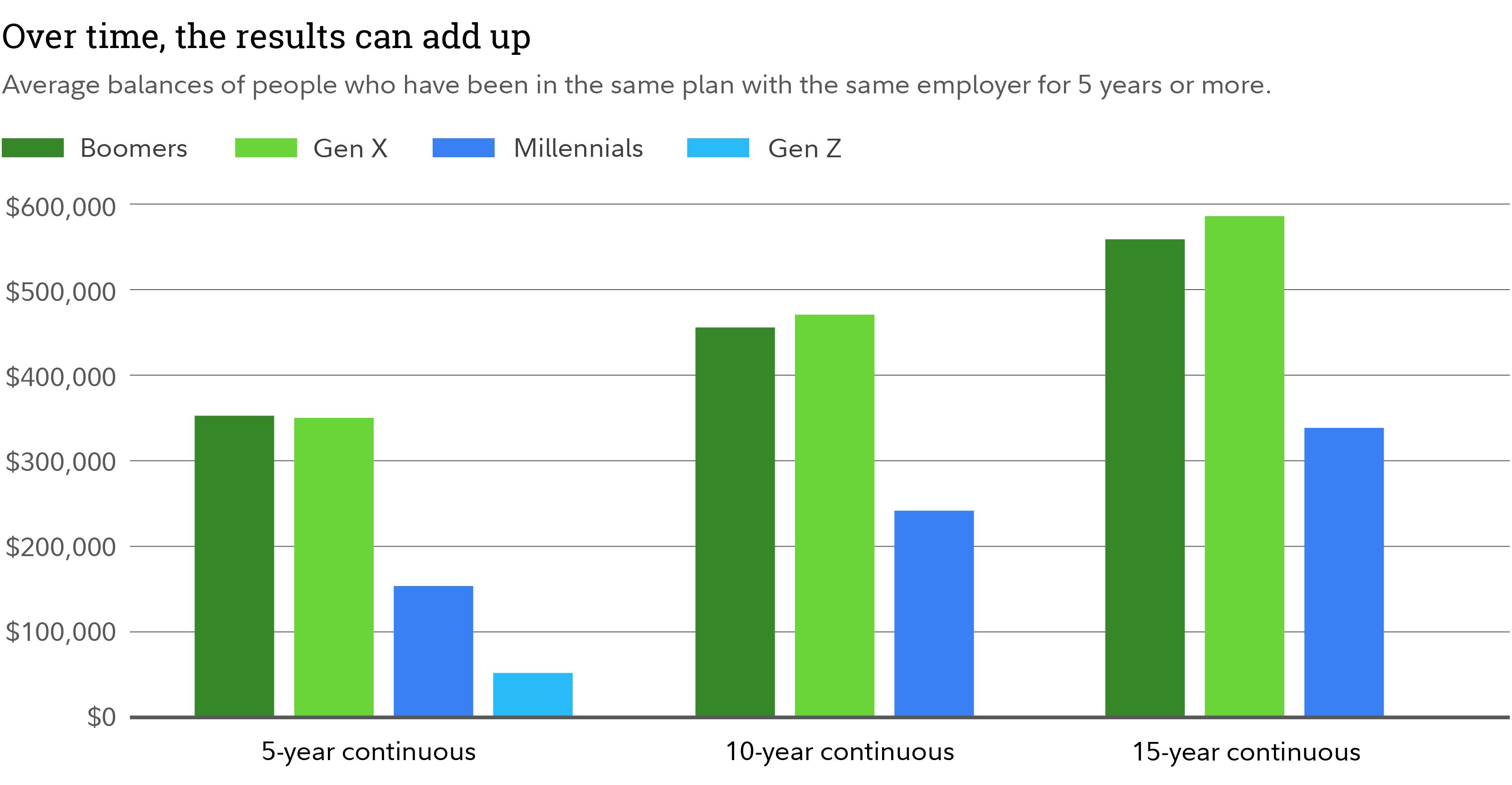

The Power of Consistent Investing

One of the most effective ways to build wealth for retirement is through steady, long-term investing. People who consistently contribute to their workplace retirement plans over many years tend to accumulate significantly higher balances. Maintaining contributions even when changing jobs is crucial to avoiding setbacks. If you switch employers, try to keep your retirement contributions at the same level (or higher) than before.

If you’re behind, don’t panic. Retirement planning is a long-term journey, and it’s never too late to improve your savings strategy.

How to Increase Your Retirement Savings

1. Save at Least 15% of Your Pre-Tax Income

Financial experts recommend saving at least 15% of your income annually for retirement. This figure includes contributions to your 401(k), IRA, and other retirement accounts, as well as employer matches. If you’re currently saving less than this, consider increasing your contributions gradually.

2. Invest for Growth Potential

While saving is important, ensuring your money grows is just as critical. Investing in assets that outpace inflation can help maintain your purchasing power in retirement. A diversified mix of stocks, bonds, and other investments tailored to your risk tolerance and age can accelerate your savings.

3. Aim to Save 10 Times Your Income by Age 67

Fidelity suggests using the following savings multiples to stay on track:

- Age 30: 1x your annual salary

- Age 40: 3x your annual salary

- Age 50: 6x your annual salary

- Age 60: 8x your annual salary

- Age 67: 10x your annual salary

If you plan to retire earlier than 67, you may need to save even more.

4. Take Advantage of Retirement Account Options

Choosing between a 401(k) and an IRA can be tricky, but both offer unique benefits:

- 401(k): Higher contribution limits and potential employer matches make this a great first option.

- IRA: Provides a wider range of investment choices and may offer tax advantages based on your income.

If your employer offers a 401(k) match, contribute enough to get the full match before considering additional IRA contributions.

5. Increase Your Contributions Over Time

Whenever you receive a raise or bonus, consider allocating a portion of it to your retirement savings. Even a 1-2% increase in contributions each year can make a significant impact over time.

6. Utilize Catch-Up Contributions After Age 50

If you’re 50 or older, take advantage of catch-up contributions. The IRS allows individuals over 50 to contribute extra to their 401(k) and IRA accounts, providing an excellent opportunity to boost savings before retirement.

Final Thoughts

Comparing your retirement savings to others can offer perspective, but it’s not the only measure of success. If you don’t reach Fidelity’s guideline of 10 times your salary by age 67, remember that any amount saved is better than none. The key is to stay consistent, invest wisely, and make adjustments as needed. By taking small, proactive steps today, you can build a more secure and comfortable retirement for the future.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/are-you-on-track-assessing-your-retirement-savings-and-strategies-to-grow-your-nest-egg.html