With 2025 well underway, investors and taxpayers alike are faced with uncertainties surrounding the global economy, stock market volatility, and interest rate fluctuations. While we cannot predict the future, we can take proactive steps to control one critical aspect of our financial lives—taxes. Thoughtful tax planning can help minimize your tax burden and maximize your savings.

Below are seven tax-efficient strategies to consider implementing early in the year, allowing you to keep more of your hard-earned money and grow your wealth over time.

1. Seize Available Deductions

This year brings good news for taxpayers: The IRS has widened tax brackets and increased the standard deduction, potentially reducing tax liability for many individuals.

- Tax bracket adjustments allow more taxable income before reaching a higher tax rate.

- The standard deduction for 2025 has increased to $30,000 for married couples filing jointly (up $800) and $15,000 for single filers (up $400).

- Itemized deductions may still be beneficial for some taxpayers, including state and local taxes, mortgage interest, medical expenses, and charitable contributions.

- Charitable giving strategies: Donating appreciated assets held longer than one year to qualified charities can provide a deduction for fair market value while avoiding capital gains tax. The deduction limit is generally 30% of adjusted gross income, with any excess carried forward for up to five years.

If you anticipate your deductions exceeding the standard amount, consider bunching deductions—such as charitable donations—into a single tax year to maximize itemization benefits.

2. Maximize Higher Savings Incentives

The government provides several tax-advantaged accounts to encourage savings, and contribution limits have increased for 2025:

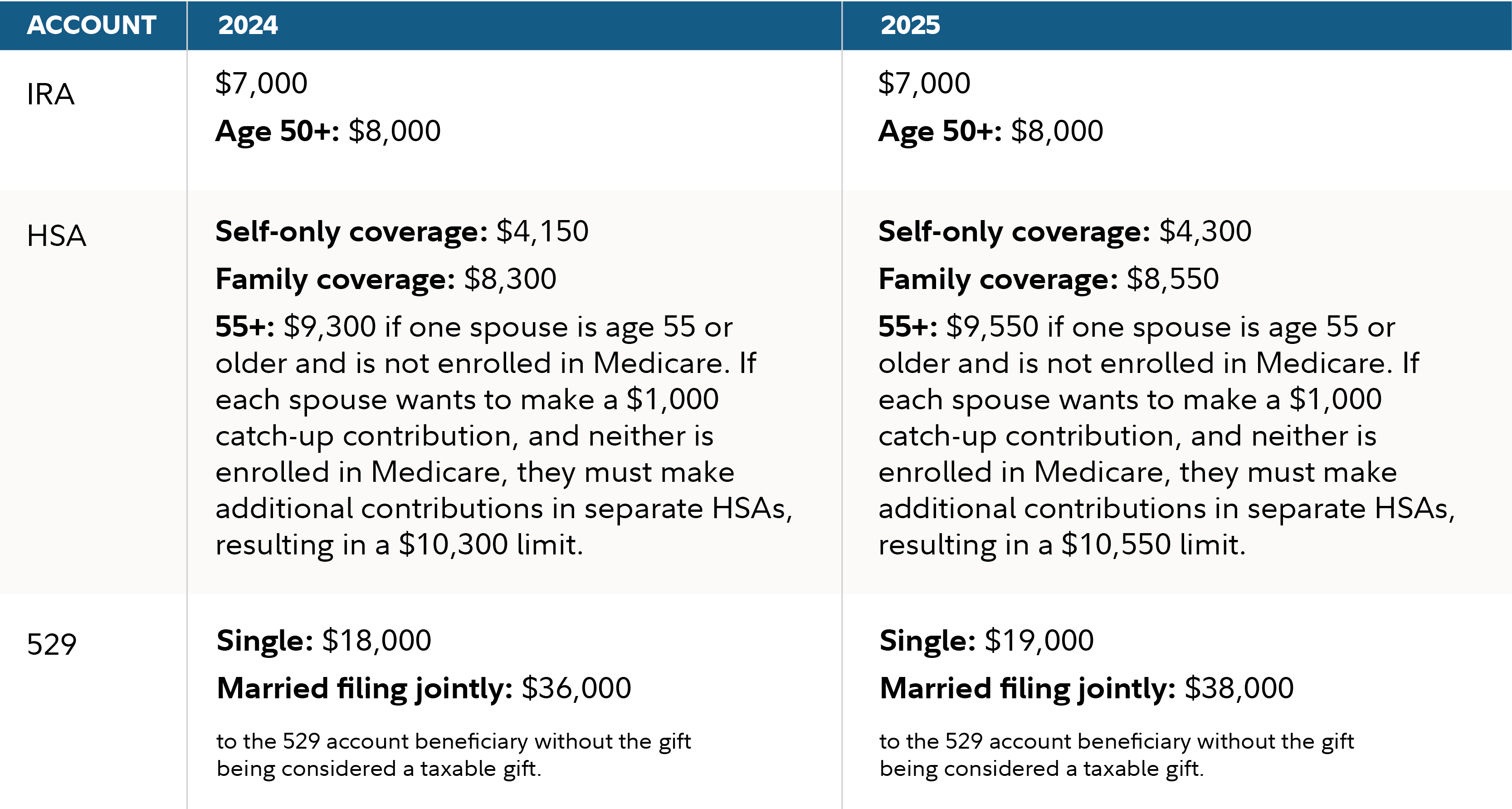

- IRA Contributions: Individuals can contribute up to $7,000 to an IRA, with an additional $1,000 catch-up contribution for those aged 50 and above.

- Health Savings Accounts (HSAs): The contribution limit is $4,300 for self-only coverage and $8,550 for family coverage, with an additional $1,000 per spouse aged 55 or older.

- 529 College Savings Plans: Contributions up to $19,000 per individual ($38,000 for married couples filing jointly) can be made without triggering the gift tax.

For those eligible, contributions to traditional IRAs and HSAs can reduce taxable income, while Roth IRA contributions grow tax-free if distribution rules are met. Making these contributions earlier in the year allows more time for tax-advantaged growth.

3. Optimize Tax-Efficient Investing

Where you hold your investments matters just as much as what you invest in. Consider these strategies for tax-efficient investing:

- Hold interest-bearing investments (bonds, CDs) in tax-deferred accounts such as IRAs to defer taxation on interest income.

- Hold stocks and ETFs in taxable accounts where long-term capital gains enjoy lower tax rates.

- Use tax-efficient funds designed to minimize taxable distributions.

By placing different types of investments in the right accounts, you can reduce taxable income while still growing your portfolio.

4. Leverage Tax-Loss Harvesting

If you have investments that have lost value, tax-loss harvesting can help offset taxable gains and reduce your tax bill. Here’s how it works:

- Sell underperforming investments to realize losses that can be used to offset capital gains.

- Offset up to $3,000 of ordinary income per year with excess losses.

- Carry forward unused losses to future tax years.

- Avoid the wash-sale rule, which prohibits repurchasing the same or substantially identical security within 30 days before or after selling it for a loss.

This strategy can be implemented throughout the year rather than waiting until year-end, ensuring better portfolio management and tax savings.

5. Consider a Roth Conversion

Converting a traditional IRA to a Roth IRA may be a wise tax move, particularly given the potential for higher tax rates in 2026 when the 2017 Tax Cuts and Jobs Act provisions expire.

- Tax now, tax-free later: You’ll pay taxes on the converted amount now, but future withdrawals—including earnings—can be tax-free if held for at least five years and taken after age 59½.

- Avoid required minimum distributions (RMDs): Unlike traditional IRAs, Roth IRAs do not require RMDs during the owner’s lifetime.

- Strategic timing: If you expect to be in a higher tax bracket later, converting in a lower-tax year can reduce lifetime tax liability.

Consult with a tax advisor to determine if a Roth conversion aligns with your financial goals.

6. Perform a Mid-Year Tax Checkup

A tax checkup can help ensure you’re on track to minimize tax surprises and optimize deductions. Key areas to review include:

- Income tax withholding: Use the IRS withholding calculator to ensure you’re not overpaying or underpaying.

- State tax withholding: Adjust if needed, especially if working remotely from a different state.

- Bookkeeping and recordkeeping: Maintain thorough documentation to maximize deductions and credits.

Remote workers should also evaluate residency options, as living in a low-tax state while working remotely could provide substantial tax savings.

7. Reassess Your Estate Plan

With the 2017 Tax Cuts and Jobs Act scheduled to expire at the end of 2025, estate and gift tax exemptions may be significantly reduced. Take action now to protect your wealth:

- Accelerate gifting: Individuals can gift up to $19,000 per recipient in 2025 without triggering gift taxes ($38,000 per married couple).

- Donate appreciated assets to reduce taxable estate value and benefit charitable organizations.

- Establish trusts for tax-efficient wealth transfer.

Revisiting your estate plan with a financial planner or attorney can help secure your legacy while minimizing future tax burdens.

The Bottom Line

Effective tax planning is an ongoing process, not just a year-end exercise. Implementing these seven tax strategies throughout the year can help reduce your tax burden, grow your wealth, and position you for financial success.

If you need personalized guidance, consider consulting a tax advisor or financial professional who can help tailor a tax-smart investment plan suited to your needs. Planning ahead today can lead to significant tax savings in the future.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/7-tax-smart-strategies-to-reduce-your-tax-bill-in-2025.html