Bad financial advice is everywhere. Some of it might come from well-meaning friends or family, some from online “experts,” and some from your own misconceptions. Falling for common money myths can be dangerous for your financial health. Whether it’s about saving, investing, or using debt wisely, misunderstanding key financial principles can lead you to make costly mistakes.

Here are six myths you need to avoid if you want to build and preserve your wealth.

Myth #1: It’s Not Worth Saving if I Can Only Contribute a Small Amount

One of the most damaging beliefs people hold is that small savings don’t matter. In reality, starting small can make a significant difference over time. This myth often discourages young people or those with limited income from saving altogether, but any amount saved can compound into something substantial in the future.

The power of compound interest allows even modest savings to grow exponentially if given enough time. Starting early—ideally in your 20s—can be key, but don’t despair if you start later. It’s never too late to begin. For example, saving 15% of your paycheck, which includes any employer match in your 401(k), could help secure your retirement.

If saving 15% seems impossible, start with what you can afford. The point is to begin the habit of saving, even if the amounts seem insignificant at first. Over time, you can gradually increase contributions. Fidelity recommends allocating:

- 50% of your take-home pay to essential expenses (housing, debt, healthcare),

- 15% of pre-tax income to retirement,

- 5% for short-term savings (for emergencies and unplanned expenses).

Remember, every little bit helps. Consistency in saving is far more important than starting with a large lump sum.

Myth #2: The Stock Market Is Too Risky for My Retirement Money

Many people fear the stock market due to its inherent volatility, believing it’s safer to keep their retirement savings in cash or low-interest savings accounts. While savings accounts protect your money from market dips, they also limit its growth. With inflation eroding the purchasing power of cash over time, a purely conservative approach can leave you with less money in real terms.

The stock market, despite its short-term fluctuations, has historically grown over the long term. Investing in a well-diversified portfolio that reflects your financial goals, time horizon, and risk tolerance is crucial for retirement planning. For young investors, having decades before retirement means they have time to weather market downturns and benefit from long-term growth.

You don’t have to be a financial expert to start investing. Many 401(k) providers offer target-date funds or model portfolios that automatically adjust your investments based on your retirement timeline. Alternatively, a managed account can help guide your investment choices.

Not investing at all is often riskier than putting money into the stock market. Over the years, the growth potential of equities can provide the kind of returns you need to retire comfortably.

Myth #3: I’m Young, So I Don’t Need to Save for Retirement Now

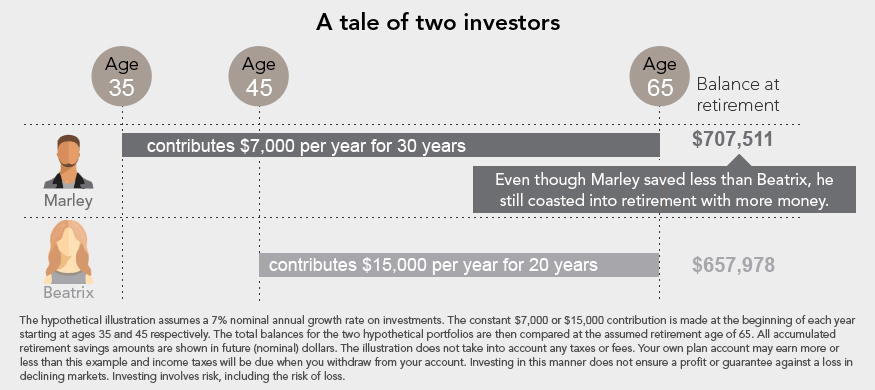

It’s easy to think that retirement is too far off to worry about when you’re young. However, this myth overlooks the critical role that time plays in wealth accumulation. The earlier you start saving for retirement, the more time your investments have to grow, thanks to the magic of compounding.

Compounding works like a snowball rolling down a hill—it picks up more snow as it grows. When you reinvest earnings from interest or dividends, you increase the base amount that can generate future returns. Over time, this leads to exponential growth. Starting early allows you to put in less while ending up with more.

For example, if you start saving in your 20s, even small contributions can result in significant growth by retirement age. Delay saving until your 40s, and you’ll need to set aside much more each month to achieve the same result.

If your employer offers a 401(k) match, take advantage of it—that’s free money. If no employer-sponsored retirement plan is available, consider opening an IRA to kick-start your savings.

Myth #4: There’s No Way of Knowing How Much I’ll Need in Retirement

Another common misconception is that retirement is too unpredictable to plan for. While it’s true that no one can predict the future perfectly, you can still make educated estimates based on general financial principles.

Fidelity provides a useful benchmark for retirement savings: By age 30, aim to have saved the equivalent of your annual salary. By 40, try to have saved three times your income. By 55, you should aim for seven times your salary, and by 67, ten times. These are broad guidelines, and your specific situation may vary depending on your retirement goals and lifestyle.

The key is to start saving consistently. You don’t need to hit every milestone perfectly, but saving regularly, increasing your contributions over time, and investing wisely will help you build a solid retirement fund.

Myth #5: All Debt Is Bad

It’s true that some forms of debt—like high-interest credit cards or payday loans—can be damaging to your financial health. But not all debt is created equal. Certain types of debt can actually be good for your finances, as they enable you to invest in your future.

For instance, a mortgage is often considered “good debt” because it allows you to purchase an asset (your home) that can appreciate in value over time. Likewise, student loans can be a worthwhile investment if they help you secure a higher-paying job in the future.

The key is to manage debt wisely. Avoid borrowing more than you can afford, and always shop around for the lowest interest rates. Make sure you’re paying off high-interest debt as quickly as possible, but don’t be afraid of using debt strategically to help achieve your long-term goals.

Myth #6: Credit Cards Should Be Avoided

Some people believe that credit cards are dangerous and should be avoided at all costs. While it’s true that irresponsible use of credit can lead to debt, when used properly, credit cards can be a powerful financial tool.

If you pay off your balance in full each month, you won’t pay interest. This allows you to take advantage of credit card rewards programs, which can offer cash back, travel points, or other perks. Many people successfully use credit cards for everyday purchases, earning rewards without ever paying interest.

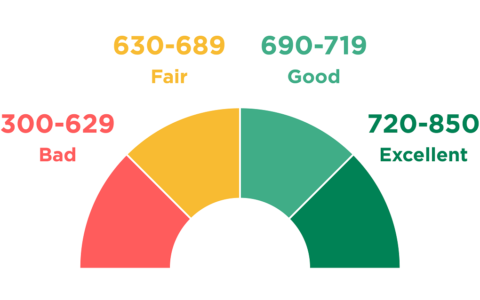

Responsible credit card use also helps build your credit score, which can be crucial when it comes time to apply for a mortgage or car loan. A high credit score can result in lower interest rates, saving you thousands of dollars over time.

Conclusion

Financial myths are pervasive, and believing them can lead you to make poor decisions that hurt your wealth in the long run. By debunking these common misconceptions, you can make smarter choices about saving, investing, and managing debt. Remember, it’s never too early—or too late—to start building a strong financial future. Start today by saving what you can, investing wisely, and managing debt responsibly.

Author:Com21.com,This article is an original creation by Com21.com. If you wish to repost or share, please include an attribution to the source and provide a link to the original article.Post Link:https://www.com21.com/6-money-losing-myths-to-avoid-dont-let-bad-financial-advice-hurt-your-wealth.html